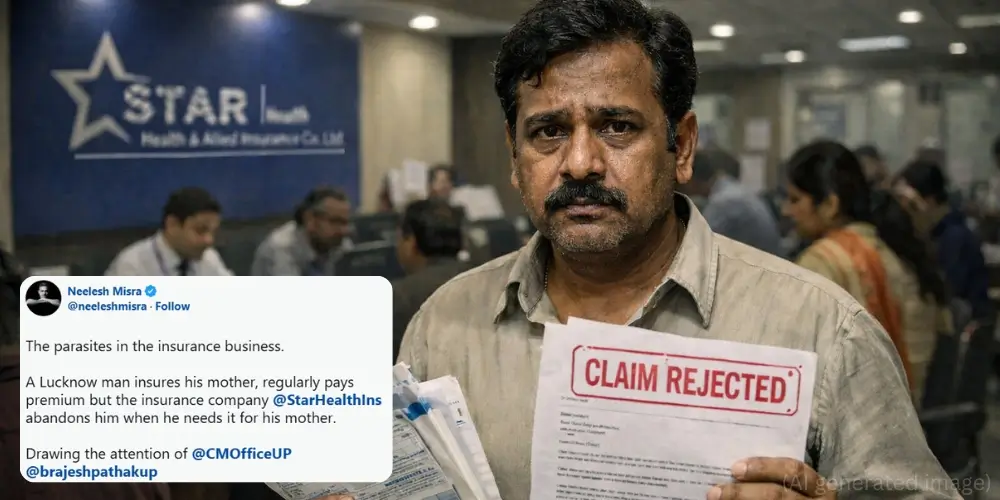

Mother’s Health Insurance Claim Rejected After Paying ₹50,000 Yearly Premium

The situation of Health Insurance Claim Rejected has once again on the public debate in India through a recent case in Lucknow. One policyholder who had been paying an annual premium of 50,000 rupees on the medical insurance of his mother claimed that the insurer did not pay for the medical emergency he needed, and the insurer refused to pay the claim, which led to frustration, social media uproar and also raised more questions about the transparency in the field of insurance.

The case went national when a renowned storyteller, Neelesh Misra, posted the issue online, which drew attention to what he termed as a disturbing behaviour by the insurer. The case indicates an increased worry by the Indian consumers with Medical Insurance Claim Rejection, the terms of the policy and the claim approval procedure.

Health Insurance Claim Denied in India: What Happened in This Case?

According to the policyholder’s statement, he approached the insurer’s local office expecting assistance after his mother fell ill. However, after hours of waiting, he was informed that the claim had been rejected. The situation reportedly worsened when an agent allegedly made an insensitive remark, suggesting that purchasing the policy was solely the customer’s decision.

The insurance company later released an official statement clarifying that claim decisions depend on documented disclosures and verified medical records. The company stated that there were indications of a potential pre-existing medical condition, and that required supporting documents were not submitted despite follow up communication. Therefore, the rejection was made strictly as per policy terms and regulatory norms.

Such explanations are common in Insurance Claim Dispute cases, where insurers cite non disclosure or policy exclusions, while customers feel the decision lacks transparency.

Why Medical Insurance Claim Rejection Creates Trust Issues

For most families, paying a Health Insurance Policy Premium is a long-term financial commitment intended to provide security during emergencies. When a claim is denied, especially after years of premium payments, it creates emotional and financial distress.

Common reasons for Health Insurance Claim Denied in India include:

● Non-disclosure of pre-existing diseases

● Waiting period clauses

● Policy exclusions

● Documentation gaps

● Treatment not covered under policy conditions

However, policyholders often feel that insurers do not communicate these limitations clearly during the purchase stage, leading to disputes at the time of claims.

Complaint Data: How Insurers Compare

According to the IRDAI Handbook of Indian Insurance Statistics 2024–25, one major standalone health insurer received 12,186 complaints during FY 2024–25, including pending and new complaints. In comparison:

● CARE Health Insurance: 4,423 complaints

● Niva Bupa Health Insurance: 3,983 complaints

Complaints per lakh policy holders is a more suitable measure of comparison. According to the data available on the Ombudsman and the number of lives covered, the insurer in question had reported about 51 complaints against every lakh policyholders.

Whereas complaint raw figures can easily be high because of great customer numbers, grievance ratios can be more realistic in determining the quality of customer service and efficiency in processing claims.

Claim Settlement Ratio: Understanding the Numbers

The claim settlement ratio is often used by consumers to evaluate insurers. For FY 2024–25, the insurer reported a claim paid ratio of 99.81% within three months, which is considered strong but slightly lower than some competitors approaching 100%.

Another important measure is the Incurred Claims Ratio (ICR), which reflects how much premium income is paid out as claims. The insurer’s ICR increased from 66.47% in FY 2023–24 to 70.3% in FY 2024–25, indicating a larger share of premiums being used for claim payouts.

However, some competitors report higher ICR levels, suggesting greater claim outflow relative to premiums.

What Policyholders Can Do If a Health Insurance Claim Is Rejected

If you face a Health Insurance Claim Rejected situation, Indian regulations provide multiple remedies:

● File a written complaint with the insurance company’s grievance cell.

● Escalate the matter to the Insurance Ombudsman if unresolved within 30 days.

● Submit a complaint through the IRDAI Integrated Grievance Management System (IGMS).

● Approach consumer courts in cases of unfair trade practices or negligence.

Maintaining proper documentation, disclosure of medical history, and policy understanding significantly improve the chances of successful claim settlement.

Growing Need for Transparency in Health Insurance

The case points out the recurrent misalignment between the expectations of customers and the processes of the insurers. Health insurance is not just a financial product but it is insurance or safety in a bad time. Hence, the integrity of communication, ethical sales, and proper evaluation of claims in the society is crucial in keeping the populace at ease.

The healthcare cost in India is ever-increasing and the controversy in relation to Medical Insurance Claim Rejection might grow unless the insurers and regulators enhance consumer awareness and redressal mechanisms.

To policyholders, the moral of the story is just the same, comprehend the policy terms, be honest to disclose past medical records and have proper documentation at hand, since the true worth of insurance is put to the test only when a claim is made.